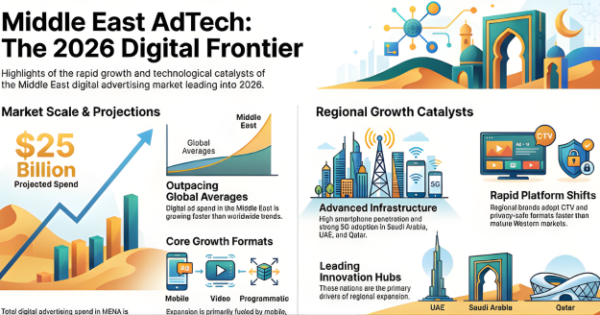

Programmatic advertising in MEA is projected to grow at a CAGR of 7.89% over the next five years, from USD 20 billion in 2025 to USD 31.6 billion in 2031, making this region one of the fastest-growing digital ad markets globally.

“But growth and market maturity are not the same thing.”

The Supply Question: Scale And Flexibility

The region’s supply challenge isn’t about quality. Our publishers produce premium inventory. The issue is that we don’t have enough of it yet, and the current structure of concentrated, guaranteed deals limits what’s possible as the market evolves.

In CTV, the constraint is real: quality inventory exists, but supply is limited. That’s about to change. Global players are launching premium ad-tier offerings in the region, which will fundamentally shift available inventory. DOOH faces a different but related challenge: we have a growing supply, but it’s fragmented and lacks standardised measurement and reporting. Buying stays siloed by market rather than regional, eliminating the data advantages that programmatic should unlock.

As supply scales, particularly with new premium CTV entering the market, the structural dynamics need to shift.

“The current model solves for simplicity and control. But it removes flexibility on all sides.”

Publishers can’t optimise yield in real-time, and buyers lose the ability to adjust targeting, creative, or frequency based on performance. The DSP tools that could drive better signal structure and data activation sit underutilised because the deal structure itself doesn’t support decision-based buying.

The next growth phase for both CTV and DOOH depends on three things: premium supply coming to market (especially new CTV ad-tiers), better signal structure that enables smarter buying, and actual data activation driving outcomes. None of that works optimally in a guaranteed-deal structure.

This doesn’t mean abandoning what exists. It means adding optionality. Flexible, outcome-driven access alongside guaranteed deals, not instead of them. When a new supply arrives, we need the mechanics in place to activate it effectively.

“Doing nothing on the supply side is not a neutral position; it is an active risk.”

Advertisers already expect more from CTV than the region currently delivers, from granular measurement to richer data signals, and when those expectations aren’t met, budgets move. CTV is also just one piece of an omnichannel strategy, and if it can’t perform, spend will simply flow to channels that can prove outcomes. In that vacuum, platforms like YouTube continue to capture disproportionate share through simplicity and incentives, while a new wave of international AVOD players enters the market ready to absorb incremental budgets. The Middle East industry risks becoming structurally sidelined while the rest of the world advances toward a more measurable, data-driven, and flexible programmatic ecosystem.

Data Activation: Moving From Campaigns To Outcomes

If we’re not connecting the dots between what users do across CTV, DOOH, podcasts, and retail, are we really reaching them, or just hoping they’ll see our ads?

Every campaign benefits from better data activation.

“The real opportunity is understanding that every user touchpoint generates data.”

Whether they’re watching their favourite series on CTV, listening to podcasts on the commute, checking football scores, or browsing retail sites, each interaction creates a signal about intent, interest, and behaviour.

That’s what data activation actually means: taking those signals across touchpoints and using them to reach the right person at the right moment with the right message. The World Cup example illustrates this. The “World Cup audience” isn’t a single segment. It’s users whose behaviour across multiple touchpoints (content, commerce, sports) indicates genuine interest. With proper data activation, buyers can identify and reach these audiences across the entire ecosystem: not just digitally, but across the growing pDOOH network in MENA and globally at airports and stadiums. A single user journey spans multiple platforms, geographies, and formats.

The cost of data activation isn’t the friction point. The friction is scale, awareness, and proven outcomes. Buyers don’t yet see enough regional success stories showing real ROI from this kind of cross-touchpoint activation. Publishers show hesitation in packaging their data for intelligent activation.

Yet, the fact is that if there’s internet access, there’s reach. Today’s programmatic ecosystem connects brands to billions of consumers across digital-first media. More importantly, it’s now capable of delivering measurable value at every stage of the journey, combining performance, efficiency, and transparency in ways that weren’t possible even a few years ago.

The capability is already here. What the market needs now is confidence, proof points, and operational alignment to fully embrace it.

Identity Infrastructure: From Capability To Adoption

MENA has enormous first-party data assets: telcos, retailers, and premium publishers, sitting largely unutilised at scale. Because there’s no unified activation framework, buyers default to Google and social. Yet this doesn’t reflect reality, given that people in MENA spend about 70 percent of their online time on the open internet – outside Big Tech’s walled gardens – across news, premium video, and audio streaming.

Globally, new identity solutions are gaining traction, but in MENA, adoption on the buy side is still cautious, and that reveals the real issue: the financial incentive isn’t obvious yet. Without demonstrated ROI and clear regional examples showing how identity unlocks better campaign precision and yield, buyers see it as a future investment rather than a current necessity.

Publishers have real monetisation opportunities available now. But until buyers understand how identity and data activation work together to drive tangible outcomes, the incentive to move remains soft.

“The gap is between capability and adoption. The pieces exist. What’s missing is proof of value at scale.”

Understanding: The Real Growth Lever

The biggest opportunity in MENA is visibility. Real growth comes from activating supply-side players and first-party data owners who want to participate but lack clarity on how biddable buying, identity, and data activation actually work at scale in this market.

Today, most conversations happen between a small group of sophisticated agencies and global buyers. But the real expansion is in the supply-side ecosystem. Publishers looking to diversify revenue streams. Data owners (telcos, retailers) looking to monetise first-party assets. These players have the assets and the motivation.

Continuous knowledge-sharing and collaboration between brands, agencies and advertising platforms will be essential to unlocking the potential of digital strategies in the region. Not only will upskilling drive business growth, but it will also foster a more innovative, future-ready industry as a whole.

The Next Episode

MENA is at a point where deliberate moves on three fronts will unlock the next phase of growth. Supply needs to evolve beyond guaranteed deals toward more flexible structures. Identity and data activation need proof points that demonstrate real ROI. And the ecosystem needs to build visibility into how these tools create tangible value.

These are market structure questions, not technology problems. And they’re solvable if we move deliberately across all three.

Farshad (Fash) Dabeshkhoy is Head of Partnerships, Africa, Middle East & Turkey (AMET), The Trade Desk

He leads strategic relationships with premium broadcasters, streaming platforms, publishers, DOOH operators and data owners across the region. Prior to joining The Trade Desk, he held senior leadership roles at Aleph, Criteo, Xandr (AppNexus), amongst others, working closely with global platforms and local

partners to develop scalable commercial and monetisation strategies. With broad experience across the ad-tech ecosystem, he focuses on building sustainable, outcome-driven partnerships that unlock long-term value for publishers and advertisers alike.

Disclaimer: This article was originally written by the author. It is shared here for educational purposes. All rights belong to the original author.